Featured

Table of Contents

Insurance provider will not pay a small. Instead, consider leaving the cash to an estate or count on. For even more comprehensive information on life insurance obtain a duplicate of the NAIC Life Insurance Policy Purchasers Overview.

The internal revenue service puts a limitation on just how much money can enter into life insurance costs for the policy and exactly how quickly such costs can be paid in order for the plan to retain every one of its tax benefits. If certain restrictions are surpassed, a MEC results. MEC policyholders may go through taxes on circulations on an income-first basis, that is, to the degree there is gain in their policies, as well as charges on any kind of taxable quantity if they are not age 59 1/2 or older.

Please note that exceptional loans accrue interest. Income tax-free treatment likewise presumes the loan will become satisfied from earnings tax-free survivor benefit earnings. Financings and withdrawals lower the plan's cash value and survivor benefit, may cause certain plan advantages or motorcyclists to end up being unavailable and might boost the possibility the plan might gap.

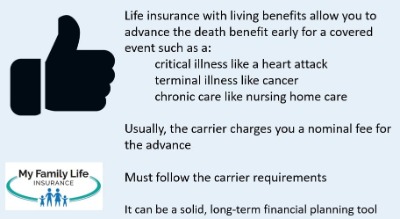

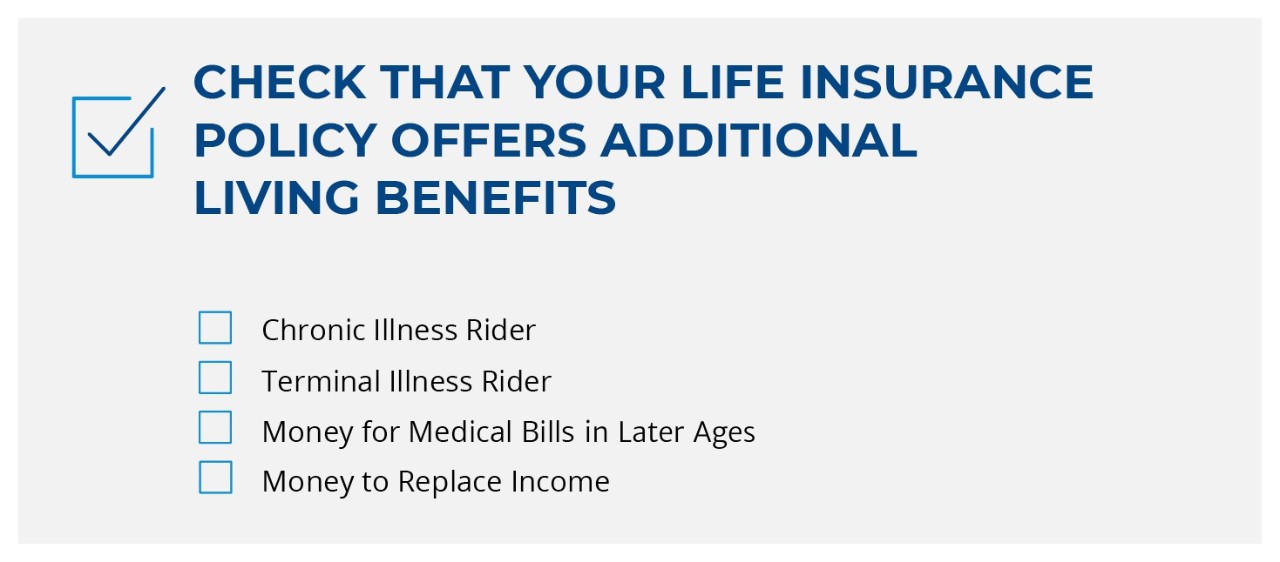

4 This is supplied with a Long-term Care Servicessm rider, which is offered for an extra cost. Furthermore, there are constraints and constraints. A client may get the life insurance policy, however not the biker. It is paid as an acceleration of the death advantage. A variable global life insurance coverage contract is a contract with the primary purpose of supplying a survivor benefit.

Why should I have Retirement Planning?

These profiles are carefully handled in order to please stated financial investment purposes. There are charges and costs connected with variable life insurance policy agreements, consisting of mortality and danger fees, a front-end lots, administrative charges, investment administration fees, surrender charges and charges for optional motorcyclists. Equitable Financial and its associates do not give legal or tax obligation suggestions.

Whether you're beginning a family or obtaining wedded, people generally start to consider life insurance policy when someone else starts to depend on their capability to gain an income. Which's terrific, since that's precisely what the survivor benefit is for. However, as you discover more about life insurance, you're likely to discover that lots of policies for example, whole life insurance policy have more than just a survivor benefit.

What are the benefits of whole life insurance? One of the most enticing benefits of acquiring a whole life insurance policy is this: As long as you pay your costs, your death benefit will never ever expire.

Assume you do not need life insurance if you do not have youngsters? There are lots of benefits to having life insurance policy, also if you're not sustaining a household.

What happens if I don’t have Premium Plans?

Funeral costs, burial prices and clinical bills can build up (Estate planning). The last thing you desire is for your enjoyed ones to bear this added burden. Irreversible life insurance policy is offered in different quantities, so you can choose a fatality benefit that fulfills your needs. Alright, this set only applies if you have youngsters.

Identify whether term or long-term life insurance policy is ideal for you. Obtain a quote of how much protection you might require, and how much it might set you back. Discover the correct amount for your budget and peace of mind. Discover your quantity. As your personal circumstances adjustment (i.e., marriage, birth of a child or job promo), so will your life insurance policy needs.

Generally, there are two sorts of life insurance coverage prepares - either term or permanent strategies or some combination of both. Life insurance companies use numerous forms of term plans and conventional life plans along with "interest delicate" products which have ended up being more widespread since the 1980's.

Term insurance policy supplies security for a given amount of time. This duration can be as short as one year or provide coverage for a specific number of years such as 5, 10, twenty years or to a defined age such as 80 or in some situations as much as the oldest age in the life insurance policy mortality.

How do I cancel Senior Protection?

Currently term insurance rates are really competitive and among the cheapest traditionally skilled. It ought to be kept in mind that it is a widely held idea that term insurance policy is the least expensive pure life insurance coverage offered. One needs to examine the plan terms meticulously to make a decision which term life choices appropriate to meet your specific circumstances.

With each new term the costs is boosted. The right to restore the policy without evidence of insurability is an essential advantage to you. Or else, the danger you take is that your health might degrade and you might be not able to get a policy at the exact same rates and even in any way, leaving you and your recipients without coverage.

You should exercise this choice throughout the conversion period. The size of the conversion duration will vary depending on the kind of term policy bought. If you convert within the prescribed period, you are not required to provide any kind of information regarding your health and wellness. The premium price you pay on conversion is generally based on your "present achieved age", which is your age on the conversion day.

Under a degree term policy the face quantity of the policy remains the exact same for the whole period. With reducing term the face quantity reduces over the duration. The costs stays the same yearly. Usually such policies are sold as home loan security with the quantity of insurance coverage decreasing as the equilibrium of the mortgage reduces.

Why is Estate Planning important?

Generally, insurers have not had the right to transform premiums after the plan is marketed. Given that such policies might proceed for lots of years, insurance firms have to use traditional death, passion and cost rate price quotes in the premium estimation. Flexible premium insurance policy, nevertheless, allows insurance companies to provide insurance policy at lower "present" costs based upon much less conservative assumptions with the right to transform these premiums in the future.

While term insurance is created to offer security for a specified time period, long-term insurance policy is made to supply insurance coverage for your whole lifetime. To maintain the premium rate level, the premium at the younger ages exceeds the real price of security. This extra costs builds a book (cash money value) which assists spend for the policy in later years as the expense of defense surges above the premium.

The insurance coverage firm invests the excess costs bucks This type of plan, which is in some cases called money value life insurance, produces a financial savings aspect. Cash values are essential to a long-term life insurance coverage plan.

{kind=link}

Latest Posts

How Does What Is A Level Term Life Insurance Policy Work for Families?

Why You Need to Understand Short Term Life Insurance

What is 30-year Level Term Life Insurance?